Research presented at Africa Games Week identified the gaps in the games industry’s infrastructure and what would help bring it to the next level

Image credit: Dr. Tegan Bristow from the Wits University School of Arts presenting her research at Africa Games Week

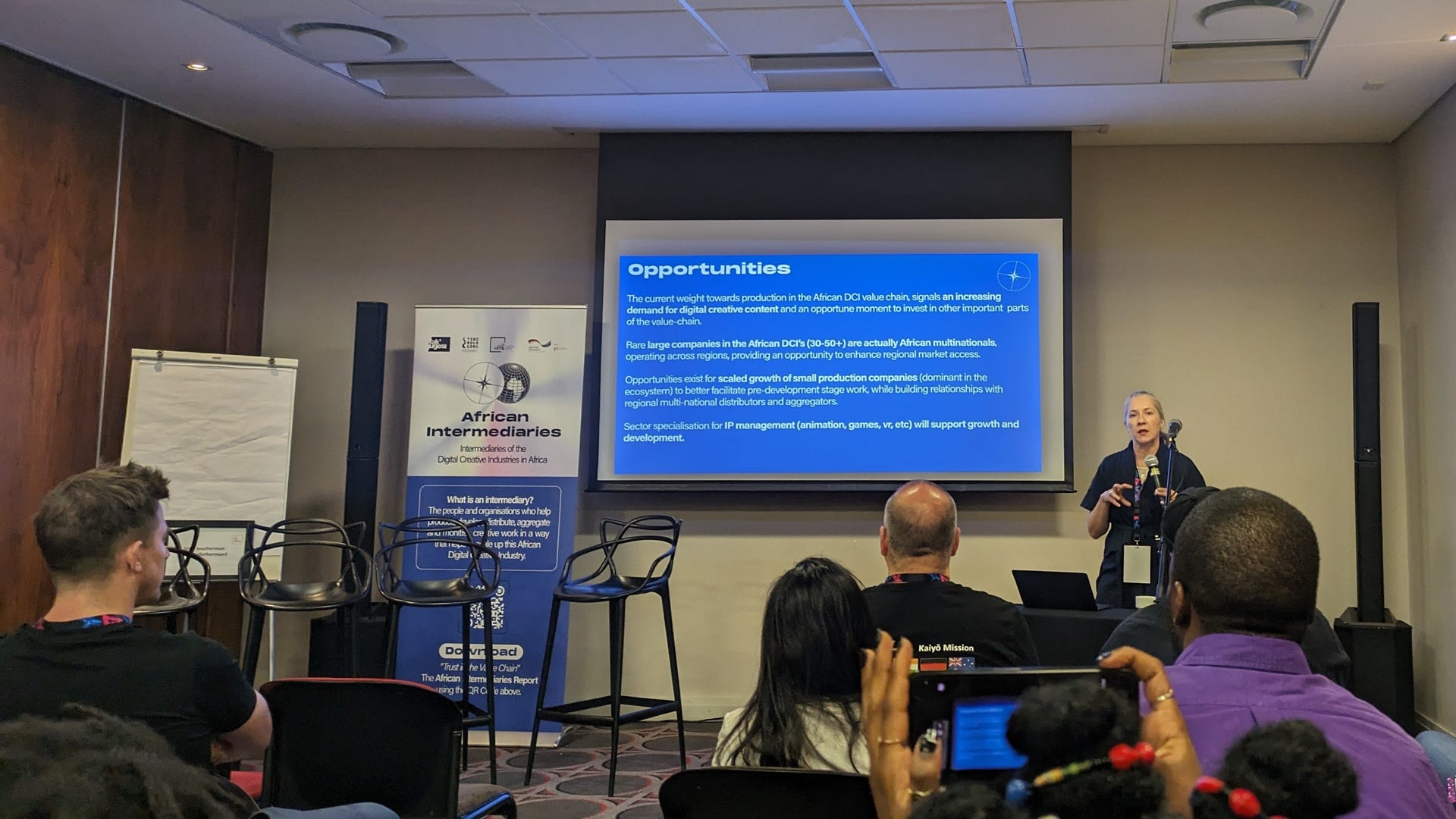

Yesterday at Africa Games Week, a talk discussed the challenges of the creative industries pipeline across Africa.

The presentation was based on new research led by Dr. Tegan Bristow from the Wits University School of Arts, in partnership with the Fak’ugesi African Digital Innovation Festival at the Tshimologong Innovation Precinct. The research particularly focused on the role of intermediaries in digital creative industries (animation and games), and mapping the gaps in the pipeline.

Bristow defined intermediaries as “the people and organisations who help produce, develop, distribute, aggregate, and monetise creative work in a way that helps to scale up the African Digital Creative Industry.” That includes the entire value chain from pre-production (incubation, funding, infrastructure development, pitching, and more), to production and distribution (established studios, publishers, distributors and so on).

The goal of the research (which you can sign up to receive on this page) was to understand the health of the African digital infrastructure, and was achieved by talking to 166 individuals from across the creative industries in 2022 to map out the current landscape and challenges of the ecosystem.

“The entire value chain within the African continent is not well considered,” Bristow said, later adding: “One of the biggest issues we have on the continent is digital infrastructure support and how digital creative industries are able to connect into that and work with that for monetisation [as well as] from a general distribution perspective.”

The research team identified five threats to the ecosystem across the African continent, starting with the fact that the value chain is heavily weighted towards production roles, leaving other aspects (pre-production and distribution) to be desired. 50% of the people interviewed identified as being in a content production role.

“People who are meant to be working in sales or marketing or distribution are actually the people producing,” Bristow explained. “This is a really, really big problem as they are trying to do more than what they should be.”

In addition, most people in the production part of the chain also identified between two and five other intermediary roles that they are holding, meaning everyone is wearing a high number of hats and not able to focus on the productions themselves.

“There’s a real issue of a lack of capacity and a lack of support in the value chain across the continent,” Bristow continued. “This indicates a crisis of role scarcity for intermediaries in the digital creative industries and an urgent need for capacities in other parts of the value chain but specifically the development stage, the market monetisation and distribution stages, and the consumer stages.”

The second threat identified by the report was the fact that the ecosystem is mostly composed of very small companies. 47% of the respondents were said to be working in companies employing between one and ten staff. In addition, only 55% reported working as registered companies.

This was linked to a lack of established infrastructure and funding across the continent that would support games production and distribution, and the scaling of existing studios.

“There’s a real issue of a lack of capacity and a lack of support in the value chain across the continent”

The third threat identified was that a lot of intermediaries are holding these roles simply because they have a need for that role and there’s no one to fill it, which Bristow described as “filling holes, not roles.”

A need for more training and bridging skills gaps were identified, though Bristow noted that a lot of the training takes place in-house or via advocacy gro

Game Industry

{kind=link}